SMM September 30, 2025 News:

Since its inception in 1953, China's aluminum industry has developed from scratch and grown from small to large, ultimately making China the world's largest aluminum producer. Throughout this process, the formation and evolution of the capacity ceiling reflect the complex interplay between China's industrialization process, industrial policy adjustments, and sustainable development. The development of China's aluminum industry can be divided into four stages:

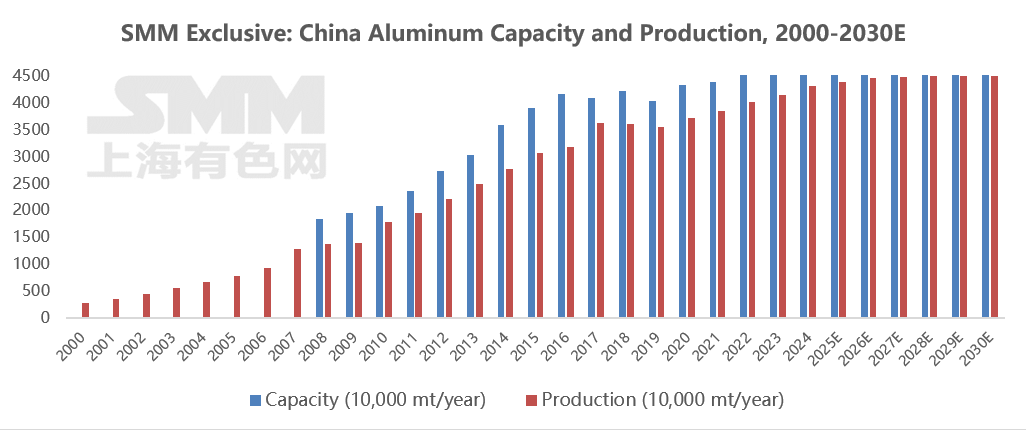

1. Initial Stage (1953-2001): New China rebuilt the Fushun Aluminum Plant with Soviet assistance, laying the foundation for China's aluminum industry. By 2001, China's annual aluminum production reached 3.42 million mt, making it the world's second-largest producer.

2. Early Unrestrained Growth (2002-2012): With the acceleration of industrialization and urbanization, demand for aluminum surged. The cancellation of the aluminum export tariff in 2002, coupled with falling international alumina prices, stimulated rapid capacity expansion. Meanwhile, growth in domestic infrastructure and real estate investment drove aluminum consumption. In 2003, the State Council issued its first document to curb overcapacity, but policy enforcement was limited, and the industry remained in an extensive development phase. Domestic aluminum production was only 4.4 million mt in 2002 but jumped to 17.8 million mt by 2010, with an average annual growth rate of nearly 20%. During this period, the export tax rebate rate was reduced from 15% to 8% in 2004, and a 5% tariff was added in 2005, curbing export-oriented capacity expansion. Simultaneously, domestic bauxite supply was insufficient, with import dependency exceeding 50%, leading to rising costs per mt of aluminum. In 2007, China's aluminum output accounted for over 30% of global production, but overcapacity led to severe price fluctuations and narrowed profit margins for enterprises. The aluminum industry was hit by the financial crisis in 2008, causing the capacity utilization rate to decline continuously, with over 1 million mt of capacity shut down that year. Overall, serious problems prevalent throughout this early stage included high energy consumption (approximately 14,000 kWh of electricity per mt of aluminum), high pollution (fluoride emissions accounting for 30% of the global total), and overcapacity (capacity utilization rate below 75% in 2009). Extensive capacity expansion after 2011 led to losses across the entire industry (2012-2016), with the capacity utilization rate remaining below 80%. 3. Supply-Side Reform Sets a Red Line (2013-2017): Existing capacity increased from 30.32 million mt to 41.64 million mt, while annual production rose from 24.95 million mt to 36.30 million mt, with growth rates consistently around 10%. In 2013, the State Council issued the "Guiding Opinions on Resolving Severe Overcapacity Conflicts," which for the first time proposed total control of aluminum capacity. In 2017, four ministries jointly launched a special campaign, clearing nearly 32 million mt of illegal and non-compliant capacity, and established a ceiling for aluminum capacity at around 45.50 million mt. This policy effectively curbed disorderly expansion through a "capacity replacement" mechanism (where building 1 mt of new capacity requires retiring 1 mt of old capacity). The policy formally set a red line of 45.50 million mt for aluminum capacity, eliminated 6 million mt of illegal capacity, and strictly controlled new capacity. In the same year, green transformation began to take shape, with Yunnan initiating capacity replacement leveraging its hydropower resources. By 2018, the share of hydropower-based aluminum exceeded 20%.

4. Deepening Constraints of Green Transformation (2018–Present): Existing capacity increased from 42.12 million mt to around 45.50 million mt, while annual production rose from 36.09 million mt to 43.12 million mt (as of the end of 2024), and the capacity utilization rate gradually climbed to over 90%. As carbon peaking gained momentum, the domestic ceiling for aluminum capacity became more firmly established. The 2024 "Action Plan for Energy Conservation and Carbon Reduction in the Aluminum Industry" requires strict implementation of aluminum capacity replacement, stipulating that new and expanded aluminum projects must meet benchmark energy efficiency levels and Class A environmental performance standards, while new and expanded alumina projects must achieve advanced levels of mandatory energy consumption limits. By the end of 2025, the share of recycled metal supply is expected to reach over 24%, and the proportion of direct alloying of liquid aluminum is targeted to increase to over 90%. Also by the end of 2025, the share of aluminum capacity meeting or exceeding benchmark energy efficiency levels is expected to reach 30%, and the proportion of renewable energy usage is set to exceed 25%. The 2025 "Implementation Plan for High-Quality Development of the Aluminum Industry" further proposes raising the share of aluminum capacity above benchmark energy efficiency levels to over 30%, increasing the proportion of clean energy usage to over 30%, and achieving a comprehensive utilization rate of over 15% for newly generated red mud. New aluminum capacity replacement projects must meet requirements such as an AC power consumption for liquid aluminum not exceeding 13,000 kWh/mt and Class A environmental performance. The use of 500 kA or larger pots is encouraged, along with the relocation of aluminum capacity to regions rich in clean energy and with available environmental and energy capacity. Efforts will also focus on strengthening research, demonstration, and application of disruptive technologies such as low-carbon smelting.

In the long term, China's aluminum capacity will be driven by multiple factors including policy constraints, energy transition, technological breakthroughs, and market demand, exhibiting a core trend of "strict total control, structural optimization, and quality leap."

1. Rigid constraints on total capacity, with optimization of existing capacity becoming the main theme. From 2025 to 2030, the average annual growth rate of capacity is expected to be less than 0.5%, with production growth mainly relying on technological upgrades of existing capacity and improved adaptability to green electricity. Capacity in traditional coal-power-aluminum provinces such as Shandong and Henan is gradually shifting to green electricity-rich regions like Yunnan and Inner Mongolia.

2. Accelerated green electricity substitution, fundamental transformation of the energy structure. Under the "dual carbon" goals, the aluminum industry is undergoing a revolutionary shift from "coal dependence" to "green electricity dominance": by 2025, the mandatory green electricity consumption ratio in the aluminum industry is set to exceed 25%, rising to 30% by 2027. Hydropower bases in Yunnan and Sichuan already achieve over 80% green electricity usage through the "aluminum-power integration" model, while Inner Mongolia and Xinjiang are exploring integrated pathways of "wind-solar-storage + aluminum" leveraging large-scale renewable energy bases.

3. Speeding up substitution with secondary aluminum, formation of a circular economy system. With the advancement of "urban mining" projects, the recycling rate is expected to exceed 70% by 2030, forming a closed loop of "aluminum scrap recycling - smelting - deep processing." The target for secondary aluminum production is set to exceed 15 million mt by 2027.

4. Deepening technological iteration, comprehensive enhancement of industry competitiveness. Technological innovation will drive the aluminum industry's transformation from "high energy consumption" to "high technology." The proportion of large prebaked pots of 400 kA and above has exceeded 90%, while 600 kA+ ultra-large pots have achieved scaled application, increasing single pot capacity by 30% and reducing land use by 20%.

5. Intensified international competition, strengthened voice in the global supply chain. China's aluminum industry is shifting from "scale expansion" to "value output." Enterprises such as Chalco and Weiqiao are investing in bauxite and aluminum projects in Guinea, Indonesia, and other countries, building a chain of "overseas resources - domestic processing - global sales."

6. Policy stimulus package in effect, continuous optimization of the industry ecosystem. Policy regulation will run through the entire transformation process of the aluminum industry, strictly controlling capacity in key air pollution prevention areas and encouraging cross-regional capacity replacement. The long-term transformation of China's aluminum industry is, in essence, a systematic restructuring of the energy mix, production methods, and industrial ecosystem. Through the substitution of green electricity, recycling, technological breakthroughs, and global deployment, the industry will not only safeguard national resource security but also provide a "Chinese solution" for the low-carbon transition of energy-intensive industries worldwide, ultimately achieving a historic leap from a "large aluminum-producing country" to a "strong aluminum-producing country."

The transformation of China's aluminum capacity is by no means a "minor adjustment within the industry," but rather a "multi-dimensional strategic initiative" that serves the national "dual carbon" goals, ensures energy and resource security, supports the upgrading of the manufacturing sector, and facilitates participation in global governance. At its core, it involves transforming a traditionally energy-intensive industry into a modern, "low-carbon, efficient, and high-value-added" sector. This not only paves the way for China's industrial transformation but also offers a "Chinese model" for the sustainable development of energy-intensive industries globally, ultimately achieving resonance between "industrial upgrading" and "national strategy."